Comparing Property and Shares: Which Investment Is Better?

It’s an age-old debate. Both real estate and stocks can build wealth, but they work in different ways. Let’s explore the differences in terms of returns, risk, tax, and leverage to help you make an informed decision.

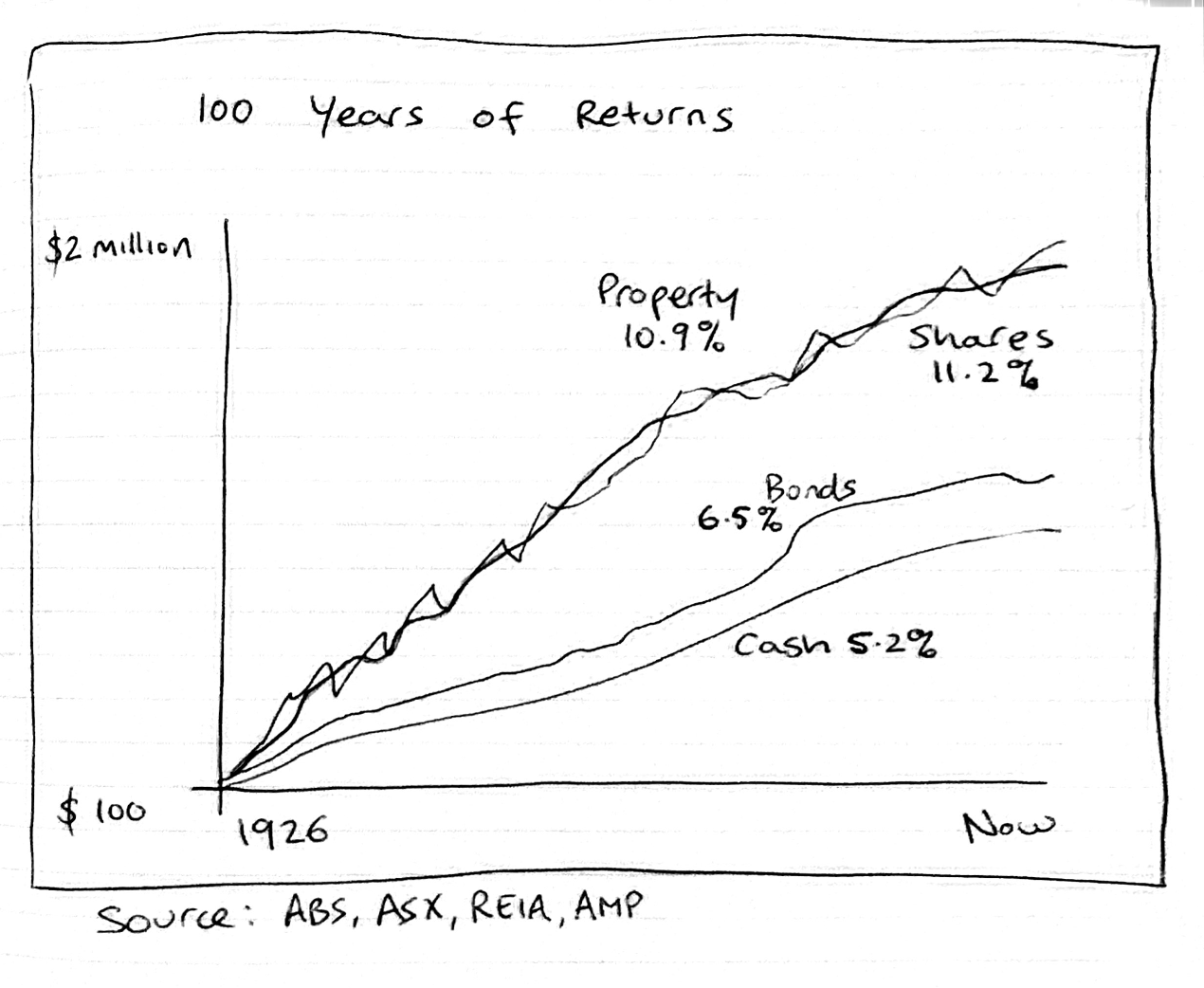

Long-Term Returns: Real Estate vs Stocks

Historically, both real estate and equity investments have produced strong long-term returns. Property provides rental income and capital growth, while shares can deliver dividends and price appreciation.

The graph above illustrates how $100 invested many decades ago grows differently depending on the asset class, with both property and shares outperforming bonds and cash.

Stability and Risk in Property and Share Investing

Property tends to be more stable because homes are often owner-occupied and market reactions are slower. Shares can be more volatile, reacting quickly to market news or economic events.

Key takeaway: Real estate offers stability, while shares provide liquidity and faster potential gains.

Tax Benefits: Equities vs Property

Both asset classes have tax advantages. Long-term holdings may qualify for capital gains tax discounts. Shares provide franking credits, whereas property can allow negative gearing and other deductions.

Leverage and Buying Power: Investing Insights

One major difference is leverage. Property financing allows investors to control a larger asset with less upfront capital. This can amplify returns but also increases risk.

Shares can also be bought on margin, but the terms are generally less favorable than property loans.

Final Thoughts on Investing in Property or Shares

Both property and shares can play important roles in building long-term wealth. Property provides stability and leverage, while shares offer flexibility, diversification, and liquidity.

Consider your financial goals, risk tolerance, and time horizon. Often, the best strategy includes a combination of both.

Learn more about why choose Precium or explore investment videos for deeper insights.

For official guidance, visit the Reserve Bank of Australia.