How Interest Rates and Population Trends Impacted Australia’s Property Market Boom

Interest rates played a key role in Australia’s property market boom, even as population growth slowed dramatically during COVID. For 2 years, our borders were shut, immigration went to zero, and usual population growth fell. Conventional logic would suggest property markets crashed—but they didn’t.

Surprisingly, prices grew, defying predictions. Let’s explore why and how interest rates and returning expats influenced this boom.

Population Trends During COVID

Australia has around 25.75 million people, traditionally growing through immigration. Pre-COVID growth averaged 300-400k per year, with 160k-200k from migration and the rest from natural increase. During border closures, growth fell sharply (ABS migration data).

- Overseas migration 2020-21 – net loss of 88,800 people, the first loss since 1946.

- Every state and territory recorded declines in net overseas migration in 2020-21.

Previously, high migration was often cited as a reason for property price increases due to population pressure. However, the 2020-21 boom shows prices can rise independently of population growth.

Returning Expats and Rental Demand

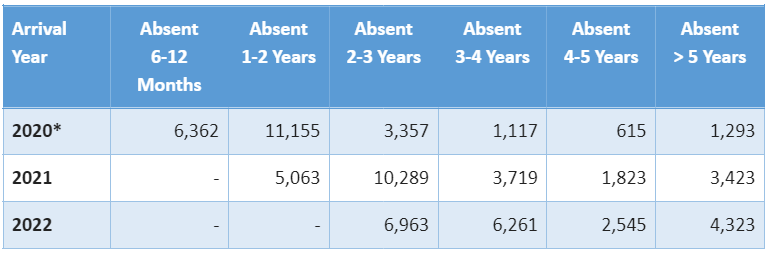

Many Australian expats returned home during COVID, creating unmeasured demand. Border Force statistics reveal:

Returning Australian Citizens

*See Footnote for Caveats from ABF

By the numbers:

2020 – 23,899 returned.

2021 – 24,317 returned.

2022 (Year to date) – 20,092 returned.

This totals 68,308 returning expats—higher-income professionals ready to rent or buy, contributing to increased demand especially in city and coastal areas.

The combination of returning expats and urban residents relocating regionally (“VESPAs” – Virus Escapees Seeking Provincial Australia) intensified rental competition. Empty city units from migrants who didn’t arrive amplified the trend.

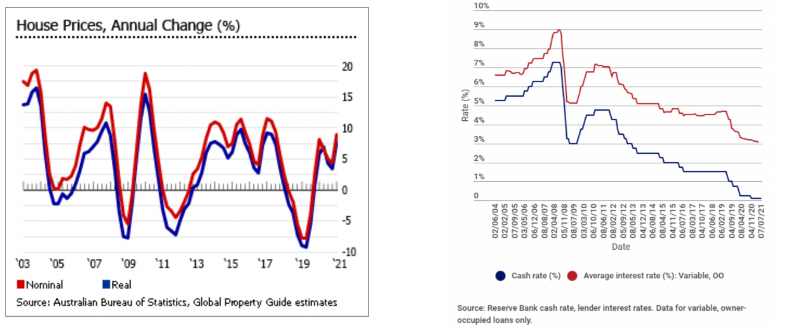

Interest Rates and Property Price Growth

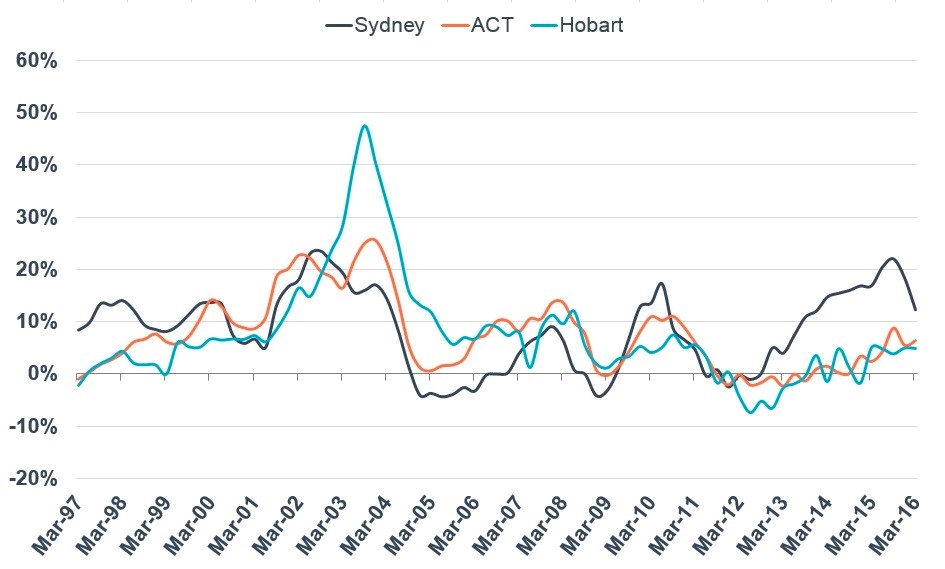

Record low interest rates are often cited as the reason property prices rise. While they influenced affordability, history shows prices can increase even when interest rates are high. Examining Sydney over the past 20 years, multiple price booms occurred at rates above 5%.

For example, Sydney saw 12.7% growth in 2010 at 7.5% interest rates, and 22.9% growth in 2003 with rates above 4.75%. Tasmania also experienced massive price spikes in 2002-2004 without population booms or ultra-low rates.

Media Myths and Market Drivers

Media often blames single factors like migration, grants, or foreign investment for property price changes. Yet these explanations rarely capture the full picture. Human demand, supply shortages, building delays, and interest rate trends collectively shape the market.

Interest rates will fluctuate, migration will ramp up, and buyer behavior will remain unpredictable. But properties in high-demand locations, coastal areas, or near major cities continue to offer strong investment potential.

Key Takeaways

- Interest rates influence but don’t solely drive property prices.

- Population growth isn’t always the main factor behind price booms.

- Returning expats and urban-to-regional migration increased rental and purchase demand.

- Supply shortages remain a core driver of property market trends.

For further insights on property investment strategies, check out our blog and video resources. To explore our services, visit Why Choose Precium.

Footnote:

ABF Disclaimer:

Caveat:

· The generally accepted definition of an expat is someone living overseas for an extended period.

· The table above counts Australian citizens returning after 20 March 2020 following extended absence.

· Figures may include dual nationals normally residing overseas.